What are Medicare Advantage Plans

Medicare Advantage plans were created under the Balanced Budget Act of 1997 and signed into law by President Bill Clinton. These plans are commonly called Part C of Medicare or some doctor’s offices call them Medicare replacement plans.

Congress designed this program to give Medicare beneficiaries a lower-premium option than Medigap. They also have very little Medicare underwriting. This means they are a coverage option for people who missed their open enrollment window for Medigap and now cannot qualify for Medigap due to health conditions.

How Medicare Advantage Works

A Medicare Advantage plan is a private Medicare insurance plan that you may join as an alternative to Medicare. Members get their benefits from a private insurance company instead of original Medicare. When you do, Medicare pays the plan a fee every month to administer your Part A and B benefits. You must continue to stay enrolled in both Medicare Part A and B while enrolled in your Medicare Advantage plan. Medicare pays the Medicare Advantage company on your behalf to take on your medical risk. This is how Medicare Advantage plans are funded.

You will present your Advantage plan ID card at the time of treatment. Your providers will bill the plan instead of Original Medicare. Again, this is also why some providers consider them Medicare replacement plans, but it’s important to remember that you can always return to Original Medicare during a future annual election period.

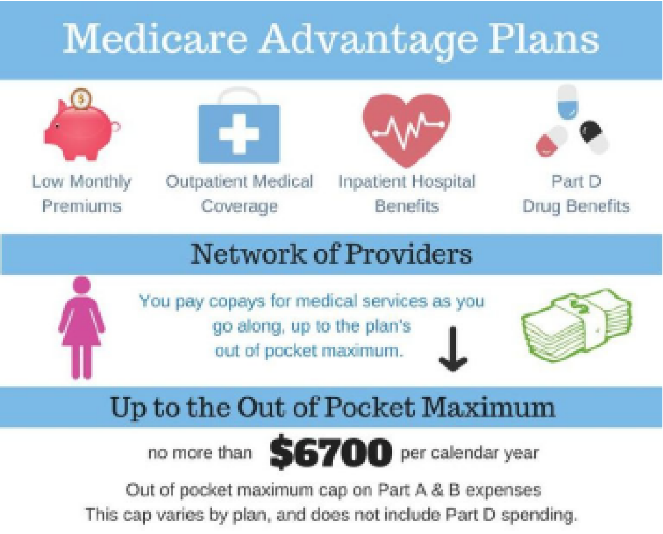

Each Advantage plan has its own summary of benefits. This summary will tell you what your copays will be for various healthcare services. Your plan will offer all the same services as Original Medicare, such as doctor visits; surgeries, labwork and so on. You might pay $10 to see a primary care doctor. Specialists will often be more – a $50 specialist copay is quite common. Some of the higher copays may come in for diagnostic imaging, hospital stay, and surgeries. One neat thing about Medicare Advantage plans is that some of them offer minor benefits for routine dental, vision or hearing. Some plans include gym memberships.

Basic Medicare Advantage Rules

- You must be enrolled in both Medicare Part A & B and live in the plan service area. Some people think they can drop Part B if they enroll in Medicare Advantage. That is false! If you drop Part B while enrolled, you will immediately be kicked out of your Medicare Advantage plan.

- Medicare Advantage plans have one health question: Have you been diagnosed with End-Stage Renal Disease.

- Use network doctors and hospitals for the lowest out of pocket costs. Plans may have HMO or PPO networks. Most Medicare HMO plans do not cover anything out of network except emergencies. In PPO networks, seeing a provider outside the network will result in substantially higher spending.

- Get prior authorization for certain procedures, especially in Medicare Advantage HMO plans.

- You must obtain a referral from your primary care physician before seeing a specialist on many HMO plans.

Medicare Advantage Networks

In exchange for lower premiums that Advantage plans offer, you agree to play by certain rules. Most Medicare Advantage plans have HMO or PPO Networks. Medicare HMO networks generally require to treat only with network providers, except in emergencies. You will need to select a primary care physician. That physician will coordinate a referral if you need to see a specialist. Medicare PPO networks allow you to see doctors outside of the network but you’ll have substantially higher out of-pocket spending to do so. Some people may feel like the rules restrict or limit them in ways that are disagreeable. However, others are willing to abide by the rules if they find a plan with an attractive low premium.

It’s a personal choice. If you are deciding between Medicare Advantage and Medigap, you’ll want to consider some of the rules before you enroll.

Medicare Advantage Enrollment Periods

Medicare Advantage plans have lock-in periods. You can enroll in one during Initial Enrollment Period when you first turn 65. After that, you may enroll or dis- enroll only during certain times of year. Once you enroll in Medicare Advantage, you must stay enrolled in the plan for the rest of the calendar year. You may only dis-enroll from an Advantage plan during specific times of the year. The Annual Election Period in the fall is the most common time to change your Medicare Advantage plan. This period runs from October 15th – December 7th each fall. Changes made to your enrollment will take effect January 1. If you decide to leave a Medicare Advantage plan and return back to Original Medicare, you must notify your Medicare Advantage plan carrier.

Be sure to carefully consider these things before joining a plan:

- Not all hospitals and doctors accept Advantage plans.

- Advantage plan benefits may change every year. In September, you will receive a packet from your insurance company telling you what is changing. The plan’s benefits, formulary, pharmacy network,provider network, premium and/or co-payments and co-insurance may change on January 1 of each year

- Your enrollment is generally for the entire year. You may only dis-enroll from an Advantage plan during certain times of the year.

- If you enroll in one right out of the gate at age 65, you need to be sure you want this coverage long-term.

- Your open enrollment window to get a Medigap plan with no health questions ends at 6 months past your Part B effective date. You might not be able to get a Medigap plan later if you have health conditions because applying for Medigap later will require you answer medical questions. You can be turned down for a Medigap at that point if you are not healthy enough to qualify.

People often ask us our opinion on which plan is the best Medicare Advantage plan. This varies based on a number of personal factors. What’s right for your friend or neighbor may not be right for you. Don’t risk making a mistake on something as critical as your health insurance. We can help explain your options in detail.

Contact Rusty von Sternberg for help today at (281) 444-5412